It is the goal of the long Γ trader to have enough swings, up and down, over the life of the position to offset the continued loss of time value. In the process you buy low and sell high, again and again . . . at least in theory.

In the example provided in the last post, I chose a somewhat arbitrary 1.5% move in the SPY since the investment in the straddle involved a premium outlay of roughly 3% of the value of the underlying. More commonly, traders use some ∆ value as a reference to place their hedges; perhaps every 200-300 ∆'s. Whatever parameters you choose, the most important thing is to be consistent in your hedging. Also, hedging does not guarantee a profit since it is always possible that the underlying will not move sufficiently up and down or that it moves only in one direction. None the less, it is probably worthwhile to employ some sort of hedging methodology if you are going to trade a long straddle.

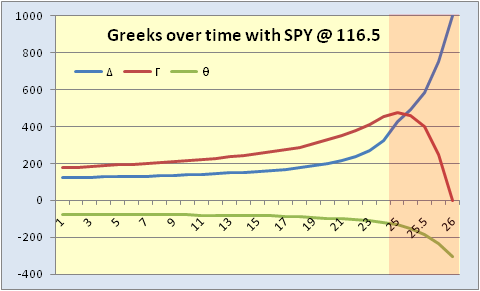

Finally, there is the consideration of implied volatility. If the stock is really not moving, then IV is likely to decline which will accelerate the option's rate of decay and negatively impact your position. On the other hand if the stock becomes extremely whippy the value of your position is likely to increase with IV up until expiration day when the options will ultimately approach values of 0 or parity. If the stock is whippy, however, there should be additional opportunities to flip the stock more frequently making it easier to cover the θ. Should IV really spike, you may also have the opportunity to close the position out on that move alone.

We will continue this discussion next time with a look at the risks of a short straddle.

No comments:

Post a Comment